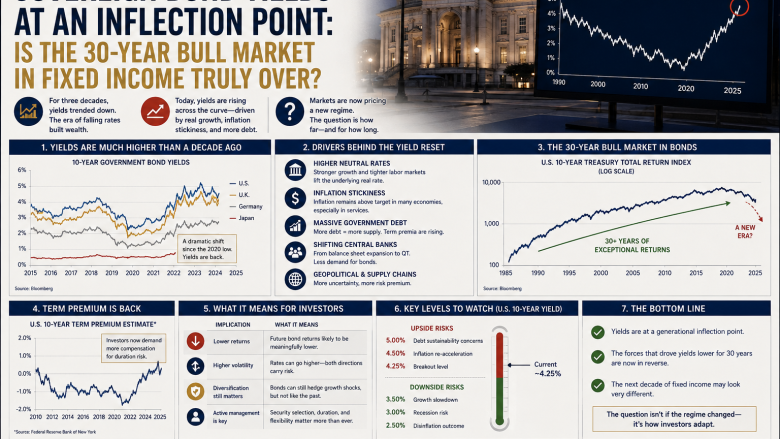

For the better part of four decades, the dominant trade in global fixed income was simple: buy bonds and wait. From the early 1980s through 2021, the multi-decade decline in interest rates created a structural tailwind for bond investors — prices rose as yields fell, generating returns that required little active management and minimal credit risk. That era ended in 2022 when the Federal Reserve began its most aggressive tightening cycle in a generation.

Three years later, the question that institutional fixed income managers are grappling with is not whether that multi-decade bull market is over — most accept that it is. The question is whether the yields available today represent fair compensation for the risks that now characterize sovereign debt markets, or whether an additional leg higher in yields lies ahead.

As of late May 2026, the 30-year US Treasury yield moved above 5% for the first time since 2007, reaching its highest level in nearly two decades, according to Goldman Sachs Asset Management’s June Market Pulse. The 10-year yield rose through Q1 2026 amid Middle East geopolitical risk and central bank expectations repricing. German Bund yields have moved in parallel. The backup in yields has challenged fixed income returns year-to-date — but the same movement has also, paradoxically, created what Goldman Sachs describes as a “compelling” opportunity set for long-term investors.

The tension between those two views — yields as risk, yields as opportunity — defines the fixed income landscape in mid-2026.

What Drove Yields Higher

Multiple forces converged to push sovereign yields to their current levels. The Federal Reserve’s hawkish hold under outgoing Chair Powell and incoming Chair Warsh kept short-term rates at 3.50%–3.75%, well above the equilibrium rates that bond markets had expected heading into 2026. The Middle East conflict — now in its third month — has kept Brent crude elevated, feeding into inflation expectations and reducing the probability of near-term rate cuts. April’s core Producer Price Index came in at 1% month-over-month, reinforcing the case for sustained Fed restraint.

The fiscal dimension also matters significantly. Goldman Sachs noted in its Q1 2026 Fixed Income Outlook that large and persistent US fiscal deficits increase bond supply, exacerbating the existing supply-demand imbalance and raising questions about long-term fiscal sustainability. “If deficits widen further, or if inflation concerns re-emerge, yields will rise again, particularly on long-dated bonds,” Goldman Sachs wrote.

The One Big Beautiful Bill Act — Trump administration tax cuts that passed Congress in 2025 — added to fiscal concerns by increasing projected deficit spending. Bond markets are simultaneously attempting to price long-run fiscal sustainability and near-term monetary policy, and the combination is producing a bear-steepening dynamic in which long-term yields rise faster than short-term yields.

Goldman Sachs on the Breakeven

Goldman Sachs Asset Management’s June 2026 Market Pulse provided one of the clearest quantitative frameworks for assessing the current bond opportunity. Its analysis shows that while the backup in yields has challenged fixed income returns year-to-date, sovereign benchmarks are offering attractive income — and rates would have to move up significantly from current levels to deliver negative total returns over the next year.

This breakeven analysis — the yield increase required for total return to turn negative, accounting for both price change and coupon income — is the critical tool for assessing whether current yields are already offering adequate compensation for rate risk. Goldman Sachs’s view as of May 29, 2026: central bank hikes appear fairly priced at this point, and if the macro backdrop were to deteriorate, policymakers have ample room to cut, creating an attractive asymmetry for long-term fixed income investors.

Goldman’s Yield Curve Strategy

In its Q1 2026 Fixed Income Outlook published January 27, Goldman Sachs articulated a steepening bias across both US Treasuries and European bonds. “Directionally, we are neutral on US Treasuries and European bonds, but hold a steepening bias across both. US steepeners could benefit in either a risk-off (labor market weakness causing front-end rates to fall) or risk-on (fiscal expansion supporting growth and pushing up long-term yields) scenario.”

This strategy reflects the unusual property of yield curve steepeners in the current environment: they function as a hedge in either direction. If growth deteriorates, the Fed cuts short-term rates while long-term rates stay anchored, steepening the curve from the front end. If growth strengthens and fiscal expansion continues, long-term yields rise while the Fed stays on hold, steepening the curve from the back end. The only scenario in which steepeners lose is a parallel shift — yields rising across all maturities simultaneously — which requires inflation to accelerate at all tenors at once.

European and UK Dynamics

European sovereign bonds face their own distinct set of pressures. The ECB held rates steady in March 2026 but raised its inflation outlook while cutting growth forecasts, citing escalating risks from the Middle East crisis. Money markets were pricing at least two ECB rate hikes in 2026 by March. ECB policymaker Joachim Nagel signaled a possible rate rise as early as one month out if price pressures persisted.

Goldman Sachs identified an additional, structural source of steepening pressure in Europe: Dutch pension funds transitioning from defined benefit to defined contribution schemes. This transition is expected to reduce duration in pension portfolios over multiple years — a non-monetary, structural source of yield curve pressure that is entirely independent of ECB policy decisions and will persist well beyond the current geopolitical cycle.

The Case For and Against

The claim that the 30-year bond bull market is definitively over deserves some precision. The structural tailwind of continuously declining yields — which generated capital gains on top of coupon income for four decades — is over. That much seems clear. The 10-year Treasury yield returning to 4%+ territory, the 30-year yield crossing 5%, and central banks globally pausing easing cycles all point toward a new rate regime that is structurally higher than the post-2008 equilibrium.

But “the bull market is over” does not mean bonds are uninvestable. At a 30-year Treasury yield above 5%, fixed income is offering nominal income levels not seen since 2007. Goldman Sachs’s breakeven analysis suggests that yields would need to move significantly higher from current levels — a scenario requiring sustained inflation acceleration beyond what is currently priced — to produce negative total returns over a one-year horizon. That framing makes current yields look more like an income opportunity than a capital loss risk.

The more nuanced argument is that active fixed income management has become more important than passive exposure. In an environment of divergent central bank policies — the Fed holding while the ECB potentially hikes, the Bank of Japan continuing its own tightening — yield differentials across sovereign markets create relative value opportunities that a passive core bond allocation simply cannot capture.

Goldman Sachs’s bifurcated approach — neutral on directionality, steepening-biased on curve structure — reflects this reality. The question is not whether to own bonds; it is which part of which curve, and for how long.

What Investors Should Watch

Four signals will define the trajectory of sovereign bond markets through the end of 2026.

The 30-year Treasury yield is the most consequential. The 5% threshold carries psychological and structural significance — it changes the valuation math for equity markets through higher discount rates, and it flows directly into 30-year fixed mortgage rates. A sustained break above 5.5% would require a significant rethink of equity market valuations at current earnings multiples of around 22 times forward earnings.

US fiscal policy signals are the second variable. The deficit trajectory under the One Big Beautiful Bill Act is a key driver of long-end Treasury yields. Congressional Budget Office projections for the 10-year fiscal outlook, and any signals about future spending or revenue changes heading into the 2026 midterms, will directly affect the supply side of the Treasury market.

Fed Chair Warsh’s June 16–17 FOMC meeting is the third. Any signal of faster quantitative tightening — beyond the current balance sheet runoff pace — would add additional supply pressure to the long end of the Treasury market, pushing 30-year yields higher even without a change in the policy rate.

Finally, 10-year breakeven inflation rates are the most direct real-time indicator of whether bond investors are pricing in further inflation risk. A sustained rise in breakevens beyond current levels would be the clearest warning signal for long-duration bond holders that another leg higher in yields is coming.

The Practical Implication for Investors

The 30-year bull market in fixed income is over in the sense that the structural tailwind of continuously declining yields has reversed. But the era of bond investing as a passive, low-maintenance allocation is not over — it is simply requiring more active management than the prior four decades demanded.

At 30-year Treasury yields above 5%, fixed income offers income levels that were unavailable for most of the past decade and a half. Goldman Sachs’s breakeven analysis suggests the risk-reward is attractive at current levels for patient investors. But that opportunity comes with genuine uncertainty: about the Federal Reserve’s policy path under Chair Warsh, about the fiscal trajectory under the current administration, and about whether the Middle East energy shock will prove temporary or persistent.

For investors building or rebalancing a fixed income allocation today, the most practical framework is income-first rather than capital-gains-first — recognizing that the 5%+ yield on 30-year Treasuries is doing real work in a portfolio, even if further price appreciation is not guaranteed. Short-duration positions offer the best risk-adjusted income with minimal exposure to the yield-rise scenario. Steepening strategies, as Goldman Sachs advocates, provide structural hedges against uncertainty in either direction. And maintaining flexibility — avoiding excessive commitment to long-duration positions until the Warsh Fed’s rate path becomes clearer — is the most consistent advice from fixed income managers surveyed through mid-2026.

The fixed income investor’s job in 2026 is not to time the market. It is to position for the asymmetry: earning meaningful income now while preserving optionality for the scenario where the macro backdrop deteriorates and central banks find themselves with substantial room to cut.

Sources: Goldman Sachs Asset Management, Goldman Sachs Global Investment Research, International Banker, Cryptobriefing, Trading Economics, European Central Bank, CME FedWatch