The gig economy has matured from a niche labor market phenomenon into a central feature of American economic life. The Bureau of Labor Statistics’ 2025 Contingent Worker Supplement estimated that approximately 36% of American workers participate in some form of alternative work arrangement — including independent contractors, gig workers, temp workers, and on-call workers — representing more than 58 million people. For many of these workers, particularly the roughly 16 million who are fully self-employed as independent contractors, navigating the financial complexities of income without employer benefits is a serious challenge that significantly affects their economic security.

The Irregular Income Challenge

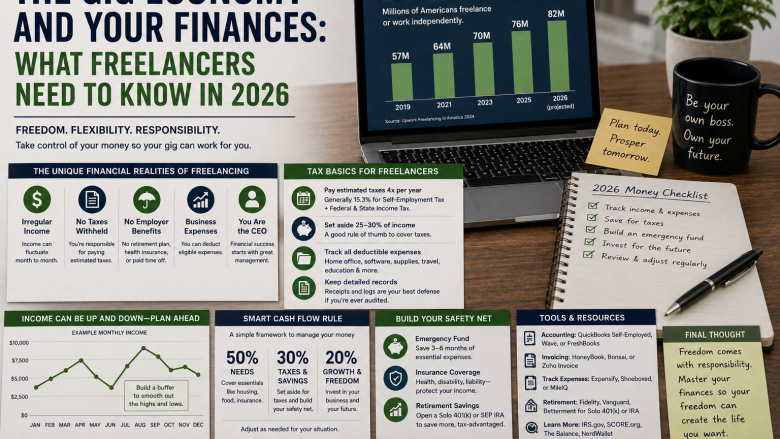

The most fundamental financial challenge for gig workers and freelancers is income volatility. Without the predictable bi-weekly paycheck that structures financial planning for traditional employees, self-employed workers must manage cash flow across periods of feast and famine — high-revenue months followed by slow months that can create real financial stress if not anticipated.

The financial planning framework for variable income differs meaningfully from the approach appropriate for stable employment. Rather than budgeting based on a fixed monthly income, the Profit First methodology — popularized by Mike Michalowicz — recommends establishing a baseline “owner’s salary” from business revenue that provides personal financial stability, holding additional revenue in dedicated accounts for taxes, operating expenses, and profit distributions, and treating highly variable income months as windfalls to be allocated carefully rather than simply spent.

The Federal Reserve’s 2025 Report on Economic Well-Being found that workers with variable income are significantly more likely to report financial stress and more likely to experience food insecurity, missed bill payments, and inadequate emergency savings than their counterparts with stable incomes — even when annual income levels are comparable. Building a buffer of 3-6 months of personal and business expenses is not a recommendation for gig workers — it is a financial necessity.

Self-Employment Taxes: The Hidden Cost That Surprises Most New Freelancers

Traditional employees pay 7.65% in FICA taxes (Social Security and Medicare) from their paycheck, with their employer paying a matching 7.65% — effectively a 15.3% total contribution split between the two parties. Self-employed individuals pay the entire 15.3% themselves as the self-employment tax, applied to net self-employment income up to $176,100 (the 2026 Social Security wage base) and 2.9% Medicare tax on income above that threshold.

For a freelancer earning $80,000 in net self-employment income, the self-employment tax is approximately $11,304 — a substantial obligation that employees with equivalent gross income do not face (though employees’ equivalent cost is hidden in the payroll tax that employers pay on their behalf rather than directing to the employee’s salary). The self-employed deduction for half of the self-employment tax — which allows freelancers to deduct from taxable income the employer-equivalent portion of SE tax — partially mitigates the burden but does not eliminate it.

Quarterly estimated tax payments are required for self-employed individuals who expect to owe $1,000 or more in federal taxes for the year. The IRS assesses underpayment penalties for insufficient estimated payments — a surprise that many first-year freelancers encounter and that can be avoided through careful quarterly planning. Safe harbor rules allow most taxpayers to avoid penalties by paying at least 100% of the prior year’s tax liability through withholding and estimated payments (110% for higher-income taxpayers).

The Business Deductions Advantage

Self-employment creates substantial tax deduction opportunities unavailable to traditional employees. Legitimate business expenses — home office, business-use portion of vehicle, professional subscriptions, equipment, software, professional development, business insurance, and a portion of health insurance premiums — reduce net self-employment income and, in turn, both income tax and self-employment tax liability.

The home office deduction requires a dedicated space used exclusively and regularly for business — a dedicated room, not a kitchen table that doubles as an office — and allows deduction of either the actual expenses attributable to that space or the IRS simplified method of $5 per square foot up to 300 square feet ($1,500 maximum). The vehicle business-use deduction can be calculated either by tracking actual vehicle expenses and applying the business-use percentage, or using the IRS standard mileage rate of 70 cents per mile for 2026 (adjusted annually).

Self-employed health insurance premiums — for the self-employed individual, their spouse, and dependents — are deductible as an above-the-line adjustment to income, reducing adjusted gross income directly. This deduction makes the cost of ACA marketplace insurance substantially more affordable for self-employed individuals in higher tax brackets.

Retirement Savings: The Biggest Financial Advantage of Self-Employment

Self-employed individuals can contribute to retirement accounts at levels unavailable to traditional employees. The Solo 401(k) allows contributions of up to $23,500 as the “employee” plus up to 25% of net self-employment income as the “employer” contribution, with a combined annual limit of $70,000 for 2026 — plus a $7,500 catch-up contribution for those over 50. The SEP-IRA allows contributions of up to 25% of net self-employment income, capped at $70,000.

For a self-employed individual earning $150,000 in net income, the maximum Solo 401(k) contribution would be approximately $37,500 in employer contributions plus $23,500 in employee contributions — $61,000 total, all tax-deductible. At a 37% marginal rate, the tax savings from this contribution is approximately $22,570 — a compelling illustration of why retirement account maximization should be among the first priorities for profitable self-employed workers.

Health Insurance: The Most Common Coverage Gap

Approximately 17% of self-employed workers are uninsured, according to the Kaiser Family Foundation, compared to approximately 8% of employed workers with employer coverage. The absence of employer-subsidized group insurance means that self-employed workers must purchase individual coverage through the ACA marketplace or professional association plans — often at significantly higher out-of-pocket cost than equivalent employer-sponsored coverage.

The ACA marketplace offers meaningful subsidies for self-employed individuals whose income falls within the eligible range, and the structure of self-employment income — which can be partially controlled through retirement contribution timing and business expense deductions — allows some workers to strategically manage their ACA-eligible income to maximize subsidy access. Working with a tax professional who understands both self-employment and ACA subsidy optimization is particularly valuable for freelancers navigating this intersection.

Building the Infrastructure for Financial Stability

Beyond the specific tax and benefit challenges, gig workers benefit from establishing several financial infrastructure elements that traditional employers provide for W-2 employees: a separate business checking account to clearly separate business and personal finances (essential for tax purposes and financial clarity), professional accounting software to track income and expenses in real time, a dedicated business savings account for tax reserves, and adequate business liability insurance appropriate to the work being performed.

The freelancer who treats their work as a genuine business — with professional financial systems, adequate reserves, and proactive tax planning — navigates the financial challenges of self-employment far more successfully than one who treats the irregular income as a supplement to be managed informally. The freedom and flexibility of independent work is genuinely valuable; the financial complexity is manageable with the right systems and professional support.

Sources: Bureau of Labor Statistics Contingent Worker Supplement 2025, Federal Reserve Report on Economic Well-Being 2025, IRS self-employment tax publications, Kaiser Family Foundation health insurance data, IRS standard mileage rates 2026, Solo 401(k) contribution limits IRS